What Do Actuaries Do

Overview:

When most people think of actuaries, they probably think that actuaries are good at math, just like the character in the cartoon picture who can solve complicated math problems and leave the audience in awe. Well, using math is just one aspect of actuarial jobs. In reality, the actuarial job is much broader than that.

Most actuaries work in a variety of insurance companies, such as life insurance companies, health insurance companies, property and casualty (P&C) insurance companies or companies that do pension business (retirement benefits). The uniqueness of the insurance industry is that once an insurance product is sold, there is a future liability that the company needs to hold at present. This future risk is a contingent event that could happen at any time in the future with any severity. Actuaries are specialized in quantifying and managing the future financial risks. Working in insurance companies is the conventional path for an actuary, however, nowadays their expertise can be utilized in other sectors/areas where risk management is needed, for example, consulting firms, banks, finance, investment, government and data science. An actuarial career becomes largely flexible as the significance of the profession is increasingly recognized and needed in any business. The actuarial profession has been frequently acknowledged as one of the best jobs. For example, the U.S. News & World Report released in 2024 ranks actuary within the top 10 in 100 best jobs and top 3 in best business jobs.

This post, along with others, focuses on the actuarial jobs and requirements in the life insurance companies in the US. The similarities could be found in other actuarial fields (e.g. health, pension, P&C).

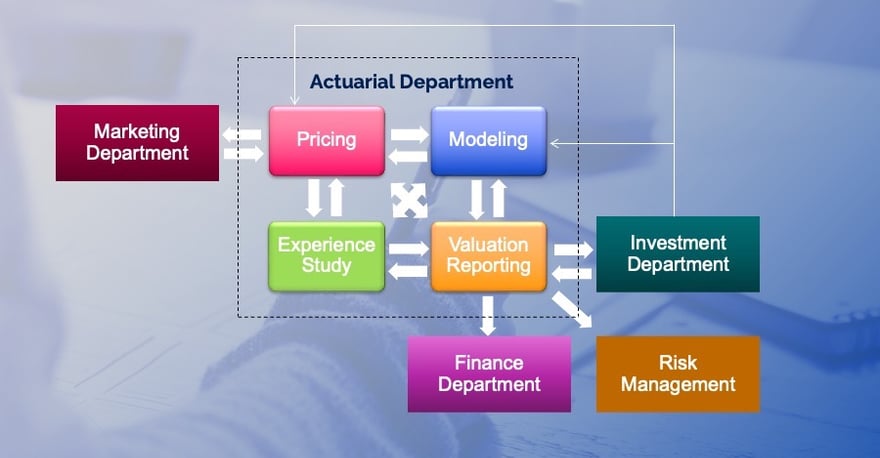

As explained above, actuaries are specialized in quantifying and managing future financial risks. They play a key role in an insurance company. The Actuarial Department led by the Chief Actuary usually includes Valuation Team, Modeling Team, Pricing Team and Experience Study Team or called Data Scientist Team. They also work closely with the Finance Department, Investment Department, Marketing Department and Risk Management Team. I drew a picture above to illustrate the collaboration across teams and departments. Please note the limitation in this picture as different companies may have different structures and even with one company the structure could change over time as explained below.

Due to the close relationship with the other departments, there are overlaps in functionalities between the Actuarial Department and others. Some companies put those overlaps under the Actuarial Department. That is why the dotted line is used in the picture to surround the Actuarial Department as the structure could change. With a professional background plus working experience in key functionalities and exposure to other departments, some actuaries take important positions (besides the Chief Actuary position) in an insurance company, including but not limited to CEO, CFO, CRO and CIO. Below are the main tasks that each actuarial team performs:

Valuation Reporting Team calculates the present value of the future liability using math (e.g. interest theory, probabilities), insurance policy information and assumptions developed by the industry or the company. The present value result is called reserve. It is the major liability on the balance sheet of an insurance company. The valuation team also performs prescribed stress testing to meet regulation requirements.

Valuation actuaries work closely with the Finance department to ensure the reserve is shown properly on the company's balance sheet.

Valuation actuaries also provide reserve results on a more granular level (e.g. by products) to the Investment department so asset funds can be invested in different portfolios to back up the liabilities. The investment team provides investment assumptions (e.g. reinvestment) to the valuation team to perform sensitivity tests.

Some valuation team includes a sub-team that calculates the Economic Capital. It is a contingent risk capital that a company needs to make sure there is enough surplus on the balance sheet to meet the stress when extreme risk events occur (e.g. pandemic, 1-in-200-year events). The actuaries would need to use probability distribution function and statistics skills to calibrate each key risk (e.g. mortality, lapse, expense) of the company. Thus, they work closely with other departments across the company to collect data, especially with the CRO/Risk Management team to ensure that risk mitigation actions will be taken.

Modeling Team develops the actuarial models using actuarial software for different purposes and different teams.

Some companies' modeling teams are centralized functions. They make model changes, update the model assumptions per market conditions, regulations and experience studies, and release the model on a regular basis (e.g. quarterly) to other actuarial teams (e.g. valuation, pricing). They work closely with each team to develop model assumptions and ensure the functionalities required by the regulations are properly modeled. In some companies, each actuarial team develops its own model.

Some modeling teams also perform financial planning and forecasting of earnings for the company. In this case, the teams will work closely with the CFO/Finance department. The investment department provides the investment information (e.g. earned rate, reinvestment) to support the task.

Some modeling teams have sub-teams called Model Governance. They perform a review and validation of the model.

Pricing Team designs insurance products.

They work closely with the Marketing department to get information on competitors and hot products in the market.

Based on the above information and the company's target profit margin, they develop product features and determine the price (i.e. premium) of the product.

They receive the asset portfolio earned rate from the Investment department on a regular basis and reset the credited rate for products with account values.

Experience Study Team develops parameters that set the key liability assumptions (e.g. mortality, lapse, expense) for the company.

They compare the experience actual data and the model projected data to determine the proper parameters for the model assumptions. They also use historic policyholder data to evaluate policyholder behavior and set the assumption for the future.

They work closely with other actuarial teams to provide the proposed changes in model assumptions.

In some companies, the experience study team is part of the valuation team. In others, when the experience study team uses lots of statistics skills, it is carved out as an independent team called the data scientist team. The data scientist team can have team members who do not have actuarial backgrounds but instead have statistical backgrounds.